US fiscal stimulus to fade, growth to ease

With the Democrats winning back control of the House, President Trump will have less scope to push through new expansionary policies. That means most of the fiscal stimulus we could have expected from the Trump administration is now probably behind us and that additional tax reductions – which would have come on top of the corporate tax cut that has helped propel US stocks over the past several months - are unlikely. As a result, economic growth is likely to stabilise at a solid, but not exuberant pace – we forecast an expansion of 2.8 per cent for next year. We think there is still a risk of inflation overshooting the US Federal Reserve’s target in 2019, but not by a significant margin.Fed rate path unchanged, dollar to weaken, yields to settle within tighter range

The changed political and fiscal landscape means the Fed will probably stick to its policy of gradual monetary tightening. Market expectations for US interest rates are now more closely aligned with the central bank's own “dot plot” forecasts, and we see nothing in the results of the mid-term elections that would alter that over the near term.

With the Trump administration unlikely to be able to secure support for further stimulative tax cuts, we expect to see downward pressure on the US dollar which, according to our currency valuation model, is trading some 18 per cent above its fair value. US bond markets should also respond positively to the reduced probability of additional fiscal stimulus. We expect the yield on the US 10-year Treasury note to trade within a range of 3 to 3.5 per cent over the coming months.

Protectionist policies to persist

When it comes to the US's stance on global trade, the impact of the elections is less obvious given that Trump can still make decisions on foreign policy and implement new sanctions or tariffs without needing the approval of the House. The implementation of tariffs have not yet had a major impact on the world economy, and our leading indicators suggest that global trade will continue to grow steadily over the next three to four months. As things stand, world exports are growing at about 4 per cent per year, in line with the long-term average.

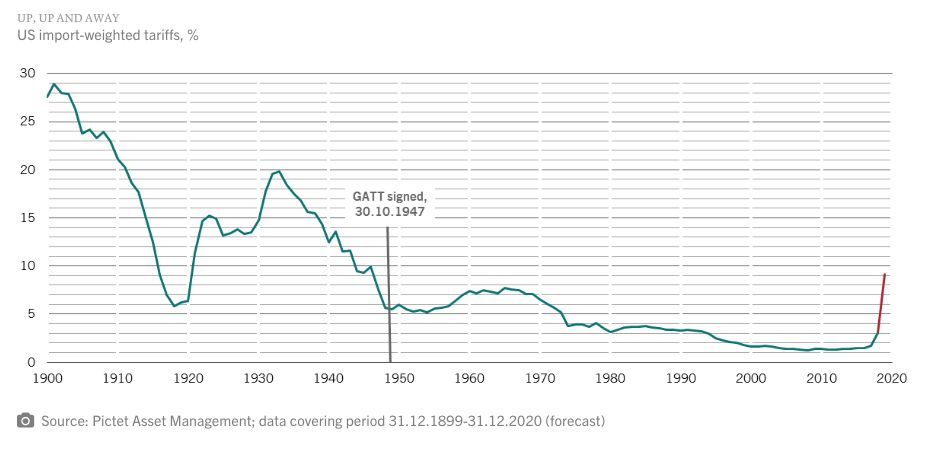

Still, it remains to be seen whether planned US import tariffs, which if implemented in full could take US import duties to levels last seen in the 1950s (see chart), will leave the world economy unscathed. Over the longer term, what really matters is continued capital investment.

Two cheers for emerging markets; stocks set for post-election boost

With the US elections out of the way, some of the concerns plaguing equity investors have faded from view. Historically, the period immediately after the mid-terms has been especially kind to stocks. This tendency and the fact that valuations for global stocks fell sharply in October, suggests equity markets could stage a healthy recovery heading into year end. Cyclical stocks such as industrials could benefit more than most.

Emerging market assets could also see a turnaround.

Developing world stocks, bonds and currencies have been hit hard in 2018 as a stronger dollar, higher US interest rates and trade disputes have weighed on investor sentiment. The mid-term elections could provide some relief. If, as we expect, the US economy’s growth cools to more sustainable levels, the risk of a renewed surge in the dollar and US bond yields recedes.

The picture is less clear when it comes to world trade – even though exports have so far proved resilient in the face of US import tariffs, President Trump shouldn't face any new hurdles in the pursuit of his ‘America First’ policy.