"The statement following the meeting noted that economic activity "has been expanding at amoderate pace," and inflation measures havemoved up "considerably but still are low.

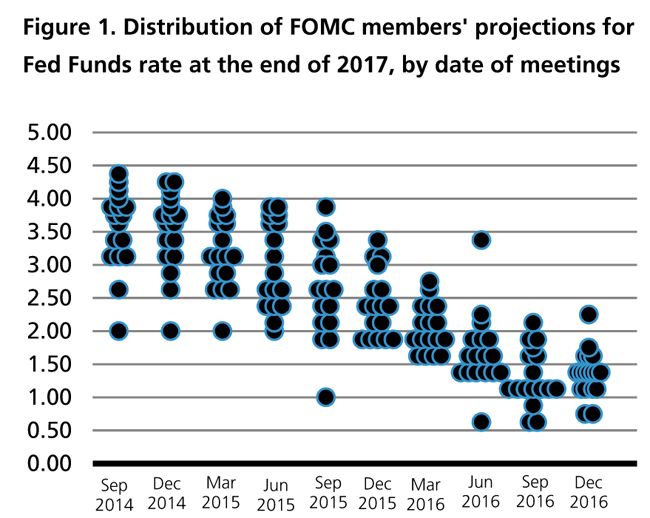

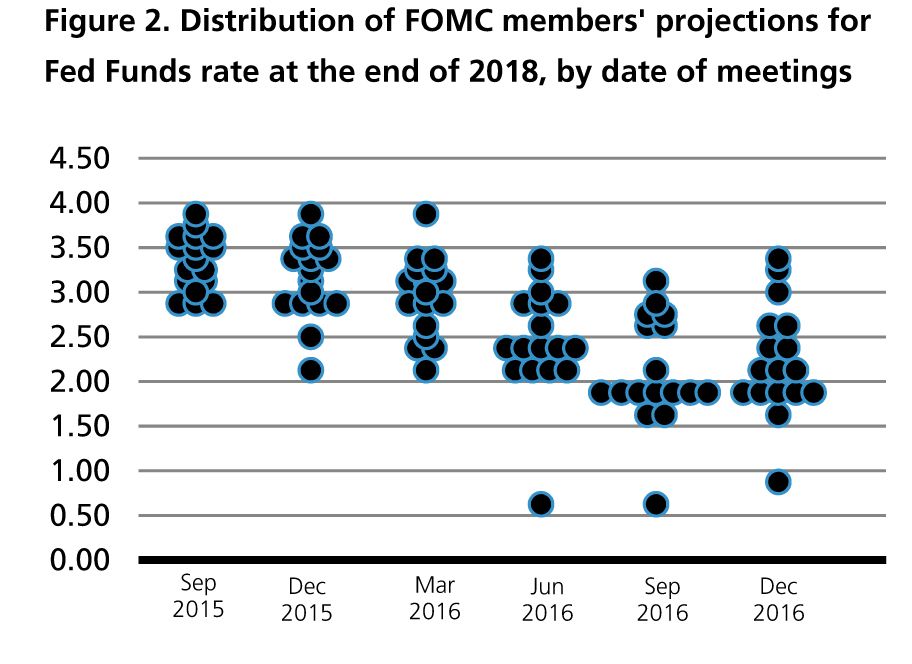

"The dot plots charts which follow, suggest Fedmembers have become slightly more hawkish. This is not necessarily surprising given the recentimprovement in economic data, continuedadvances in employment, and prospects for moreexpansive fiscal policy going forward.

Based on median estimates (Figure 1), Fedmembers now anticipate three 0.25% rateincreases in 2017 - up from the two increasespreviously projected for next year. They continueto project three rate increases in 2018 as well (Figure 2). The dot plot, which is published afterthe FOMC meeting, reflects members' opinionson where the fed funds rate should be at the endof the stated period.

Implications for Fixed Income Portfolios

Market reaction to yesterday's meeting wassomewhat contained. US interest rates driftedhigher while credit spreads remained unchanged to slightly wider. It may take sometime for market participants to digest whatwe view as a slightly more hawkish turn bythe Fed.

More broadly, the recent move higher in US interest rates in November and into December has restored term premium, and we anticipate this trend will continue at a tempered pace. The immediate impact to our fixed incomeport folios is limited given the interest rate hike was largely expected.

Against the backdrop of globally divergingmonetary policies, heightened political event risksand de-synchronized growth, we currently havemoderate active risk in our fixed incomeport folios. Many strategies remain near neutral interms of overall interest rate exposure, thus theimpact from active duration positioning has beenrelatively muted. We continue to favor interestrate exposure in Europe, Australia and NewZealand over US and Japan.

Implications for All-Equity Portfolios

In US equity markets, stocks initially rose following Wednesday's announcement, but retreated shortly after Chairman Janet Yellen'snews conference. Major indices ended the day innegative territory. Nevertheless, we do not think the Fed's recent action will have a meaningful impact on our all-equity portfolios going forward.

Implications for Multi-Asset Portfolios

In our multi-asset portfolios, we have retained along US 10-year Treasury breakeven trade which reflects the likelihood that inflation will overshoot. However, relative to German bundsand peripheral European debt, we see US nominal bonds as offering attractive carry after the recent spike in yields.

Prior to the US election, one of our highes tconviction views globally was that US inflation risks were underpriced. Therefore, the majority of our multi-asset portfolios were long inflation linked US Treasuries against nominal US Treasuries - often referred to as the 'breakeveninflation rate.' Given the significant rise ininflation expectations since the US election, webelieve the investment case for this position isclearly more balanced.

While Donald Trump's victory severely jolted thehighly consensual "lower for longer" narrativeand put fiscal policy firmly on the agenda, we donot expect the Fed to be pre-emptive in addressing rising inflation risks. Indeed, a more sustainable recovery in prices is precisely what the Federal Reserve wants.

The FOMC statement that "near-term risks to theeconomic outlook appear roughly balanced" isconsistent with last month's message, as well as the accompanying statement that came with the December 2015 rate hike. This suggests strongly to us that the Fed will lag the data and want tosee clearer signs of sustainable inflation beforehiking again. As the FOMC pointed out, market measures of inflation compensation may have shifted, but remain low. Therefore, we expect some overshooting of US inflation, and while at least some of this is now in the price of US Treasuries, we have retained thebreakeven trade.

In terms of equities, most of our multi-asset portfolios remain overweight US Value Equities.

Our analysis shows that collectively, US equitiesare overvalued, but on a sector and factor level there is very significant valuation divergence. While the valuations of bond proxies and secular growth stories (e.g. technology) became stretched amid the highly consensual 'lower forlonger' narrative, more cyclical 'Value' sectors including Energy and Financials have underperformed and now look very attractive relative to the wider market.

Historically, Value as a factor has outperformedwhen the US yield curve is steepening. Mr.Trump's victory prompted a very sharp rotation within US equities back towards Value plays as longer-dated Treasury yields spiked higher. But given the scale of the outperformance of Growth versus Value in recent years and the likelihood that inflation overshoots, we believe the reversal has further room to run.

We expect the US dollar to continue to be well supported given our belief that the Fed is likely tolet inflation rise. We see the chances of threehikes in 2017 as slightly higher than what is reflected in futures markets.

In Emerging Markets, we retain a positive bias toward equities and selected currencies.

There was some marked weakness acrossemerging market equities immediately following Mr. Trump's victory. However, we believe fears about the impact of a stronger US dollar andwider trade protectionism risks are overdone andare more than reflected in emerging market equity valuations.

We do not see a stronger US dollar as derailing the improvement in overall demand momentumin emerging markets or the earnings upgradestory. Furthermore, we see the potential boost to US growth from an increase in infrastructure spending and lower tax rates as positives for demand growth in emerging markets.

Within emerging market currencies, we haver ecently taken profits in the Russian rouble aftermore buoyant oil prices supported strong performance. We retain a long exposure to the Colombian peso, which is another currency likely to be supported by more stable energy prices, and to the Mexican peso, which we view as structurally cheap on a long-term basis."