Emerging market currencies have lost 10% this year vs. 4% during the 2013 taper tantrum. But is that really justified? In this month's EM Monitor we explore the factors behind the sell-off.

Pictet Asset Management

| 19.07.2018 10:55 Uhr

Archiv-Beitrag: Dieser Artikel ist älter als ein Jahr.

In our view, the sell-off in EM currencies since mid-April is not comparable to the 2013 taper tantrum that was triggered by a classic balance-of-payments crisis. Rather, we think it is due to four global, idiosyncratic factors that impact the currencies of both current-account-deficit (CAD) and current-account-surplus (CAS) countries:

Rising global rates/stronger USD (affecting mostly CAD)

Trade tensions (affecting mostly CAS)

Renminbi (RMB) contagion (affecting CAS & commodity exporters)

Rising populism (affecting all)

Is the correction in EM currencies justified?

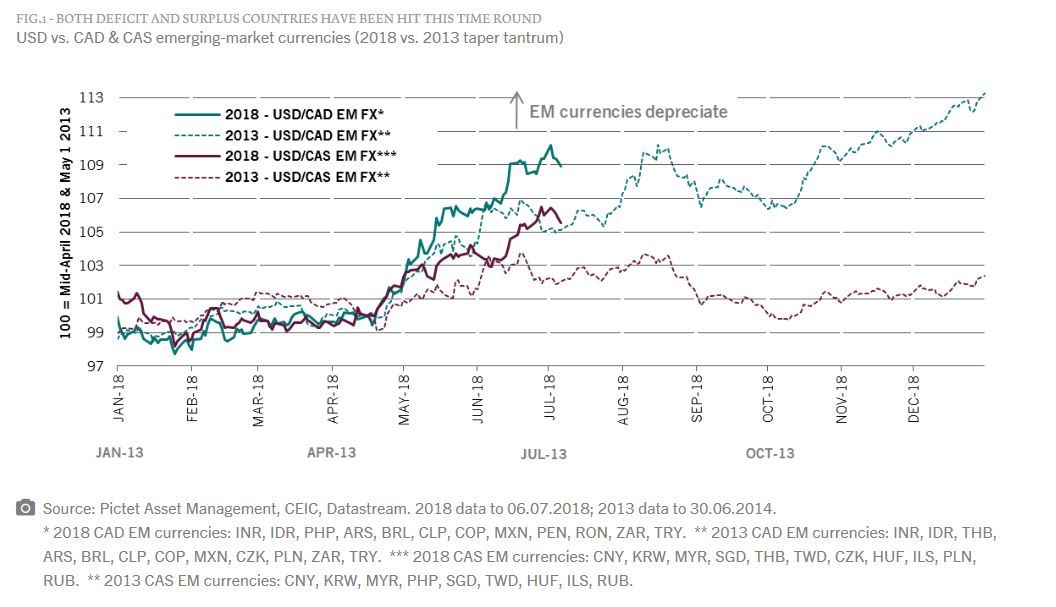

Observation 1 - A broad sell-off

EM currencies have lost 10 per cent this year, compared with 4 per cent in 2013 (Fig.1). The main difference with the 2013 taper tantrum is that the sell-off is broad-based, hitting both deficit and surplus countries.

Countries running a current account surplus have not been sheltered from the sell-off, but this is no contagion. We think it is due to trade tensions, and exposure to China and a weak renminbi.

zum Vergrößern bitte auf den Chart klicken

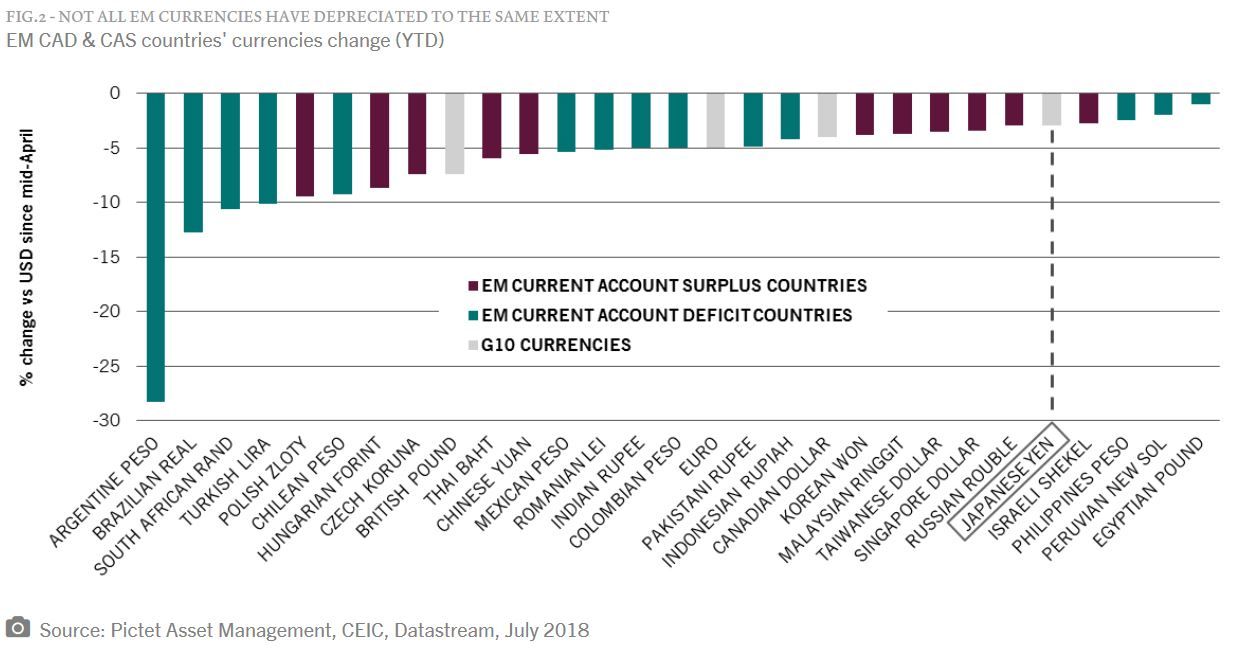

Observation 2 - Current account positions are much stronger across the board than 5 years ago

Unlike 2013, there are significant differences between countries. While some EM currencies have outperformed the most resilient of the G10 currencies, the yen, the worst performers are four main deficit countries' currencies, led by the Argentine peso (Fig.2).

zum Vergrößern bitte auf den Chart klicken

However, although countries with larger current account deficits (a proxy for higher external financing needs) typically have weaker currencies, not all CAD countries have seen their currencies depreciate as heavily this time. The main culprits are Argentina and Turkey, which exhibit genuine balance-of-payments fragility.

A point to note is that the two countries are the exception - current account deficit countries have sharply reduced their external financing needs, and appear much better placed to cope with higher rates.

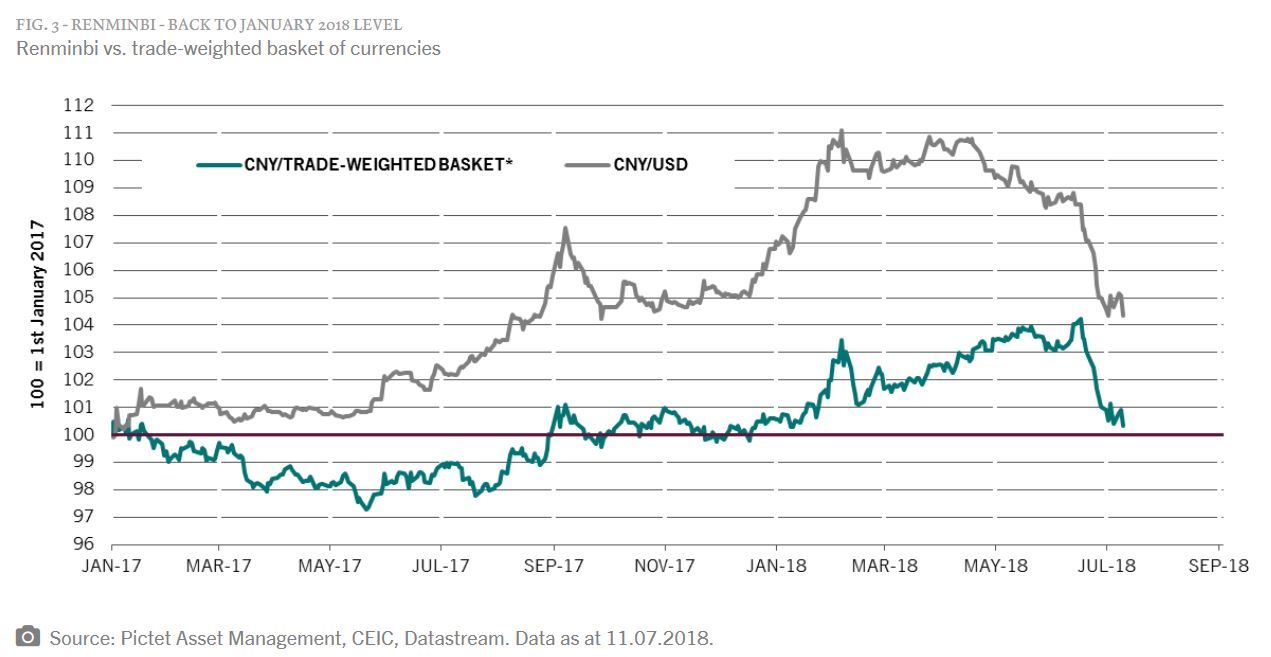

Observation 3 - No contagion to fear from China

Admittedly linked to trade tensions, the weakness of the renminbi (RMB) comes after Chinese authorities allowed the currency to appreciate by some 4 per cent (Fig.3) versus its trade-weighted basket of currencies. We think it is a welcome catch-up against main trade partners.

zum Vergrößern bitte auf den Chart klicken

A reassuring factor is that net capital outflows have been very limited year-to-date thanks to China’s improving fundamentals. Capital controls in place are also stricter since January 2017, notably on overseas direct investment, and this has reduced the risk of capital-flight panic.

Conclusion

Many emerging countries have reduced their current account deficit in recent years, putting them in a much better position to withstand external shocks. And although growth is slowing in China, its economy's fundamentals are stronger than in 2013.

Trade-related tensions remain, and the risk of a populist government is a concern in Brazil. But in our view, the correction in emerging market currencies has gone too far.

Patrick Zweifel, Chief Economist, Pictet

Performanceergebnisse der Vergangenheit lassen keine Rückschlüsse auf die zukünftige Entwicklung eines Investmentfonds oder Wertpapiers zu. Wert und Rendite einer Anlage in Fonds oder Wertpapieren können steigen oder fallen. Anleger können gegebenenfalls nur weniger als das investierte Kapital ausgezahlt bekommen. Auch Währungsschwankungen können das Investment beeinflussen. Beachten Sie die Vorschriften für Werbung und Angebot von Anteilen im InvFG 2011 §128 ff. Die Informationen auf www.e-fundresearch.com repräsentieren keine Empfehlungen für den Kauf, Verkauf oder das Halten von Wertpapieren, Fonds oder sonstigen Vermögensgegenständen. Die Informationen des Internetauftritts der e-fundresearch.com AG wurden sorgfältig erstellt. Dennoch kann es zu unbeabsichtigt fehlerhaften Darstellungen kommen. Eine Haftung oder Garantie für die Aktualität, Richtigkeit und Vollständigkeit der zur Verfügung gestellten Informationen kann daher nicht übernommen werden. Gleiches gilt auch für alle anderen Websites, auf die mittels Hyperlink verwiesen wird. Die e-fundresearch.com AG lehnt jegliche Haftung für unmittelbare, konkrete oder sonstige Schäden ab, die im Zusammenhang mit den angebotenen oder sonstigen verfügbaren Informationen entstehen.

Das NewsCenter ist eine kostenpflichtige Sonderwerbeform der e-fundresearch.com AG für Asset Management Unternehmen. Copyright und ausschließliche inhaltliche Verantwortung liegt beim Asset Management Unternehmen als Nutzer der NewsCenter Sonderwerbeform. Alle NewsCenter Meldungen stellen Presseinformationen oder Marketingmitteilungen dar.

Klimabewusste Website

AXA Investment Managers unterstützt e-fundresearch.com auf dem Weg zur Klimaneutralität.

Erfahren Sie mehr.